-

Very excited for this Kentucky Finance Conference. It’s one of my favorite “boutique” conferences; always a great set of papers and awesome discussants. I met @arpitrage here for the first time last year. Thread warning; mute if boring. uky.edu/financeconference/2019-program #KentuckyFin2019Permalink On twitter.com

♻️ 7 Retweets

❤️ 29 Favorites

Mood +6 🙂

♻️ 7 Retweets

❤️ 29 Favorites

Mood +6 🙂

-

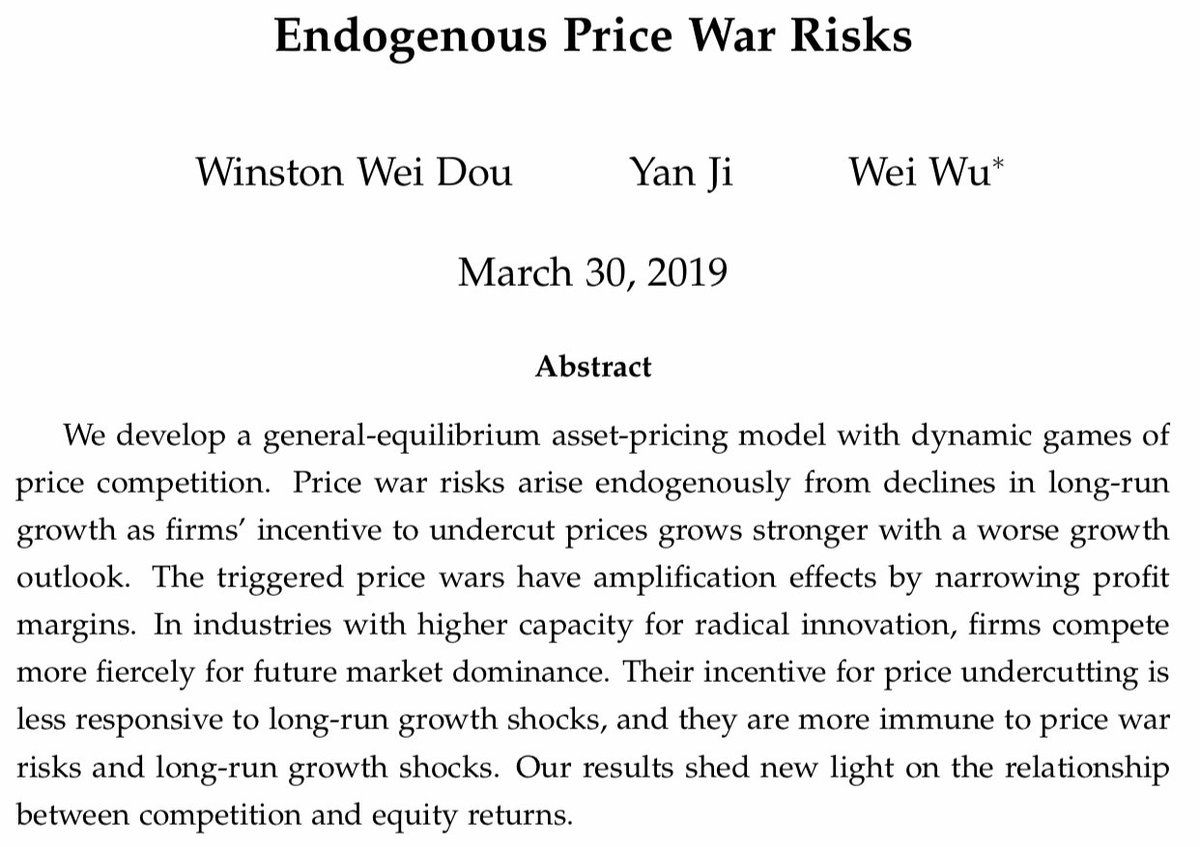

First up, “Endogenous Price War Risks” by Winston Dou (with Yan Ji and Wei Wu). Price wars are moves to a new, collusive low-price Nash Equilibrium #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 4 Favorites

Mood -2 🙁

♻️ 4 Retweets

❤️ 4 Favorites

Mood -2 🙁

-

Stylized facts: 1. (Low-frequency) consumption growth covaries with profit margins 2. There are more price wars when growth is low 3. Growth predicts profit margins particularly for low-innovation capacity industries #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 1 Favorite

Mood +10 🙂

-

Model features continuum of duopoly industries and two-layer aggregation: firm→industry→economy. Firm's have customer base (≣consumers' habits). Firms sustain tacit collusion through threat of price war. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood -4 🙁

-

Finds: When long-run consumption growth lower, market power falls, price war threat increases. Industries with more radical innovation potential (empirically, low cosine similarity of patents) less sensitive to consump growth shocks (asset pricing implications). #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +1 🙂

-

Bob Dittmar discussion praises engagement with IO foundations of asset pricing; surprising dearth of empirical evidence on drivers of cross-sectional variation in industry returns! But asks couldn't radical innovation matter for reasons other than price war risk? #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood +3 🙂

-

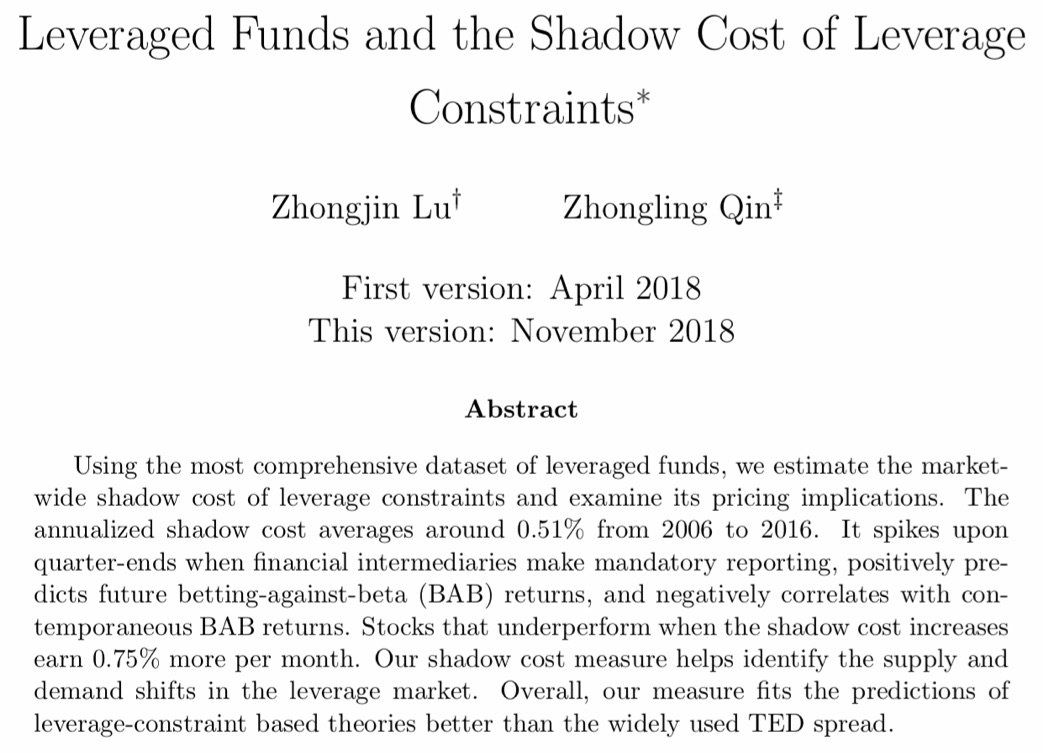

PAPER 2: “Leveraged Funds and the Shadow Cost of Leverage Constraints” by Zhongling Qin with Zhongjin Lu (UGA @TerryCollege PhD student). Marginal investor has to pay borrowing rate > risk-free rate to take on leverage. Old story, but analyze with new, good data. #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 4 Favorites

Mood +2 🙂

♻️ 5 Retweets

❤️ 4 Favorites

Mood +2 🙂

-

This paper uses comprehensive data on leveraged funds (instead of many studies' use of TED spread which is not a great proxy). VERY COOL: Estimate leverage cost by regressing fund returns on benchmark returns. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +6 🙂

♻️ 4 Retweets

❤️ 1 Favorite

Mood +6 🙂

-

Estimated shadow cost of leverage constraint is high when we would expect, predicts betting-against-beta return with the expected sign (unlike TED spread, which has “wrong” sign), and exposure to this measure seems to be priced. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood 0

-

Petri Jylhä discussion [beautiful slides!] notes tracking error implied spread (TEIS) is Leveraged ETF returns→tracking error→cost of leverage→shadow cost. First two →s mostly OK; asks about 3rd: relies heavily on assumptions (cf Gârleanu and Pedersen, 2011). #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood -2 🙁

-

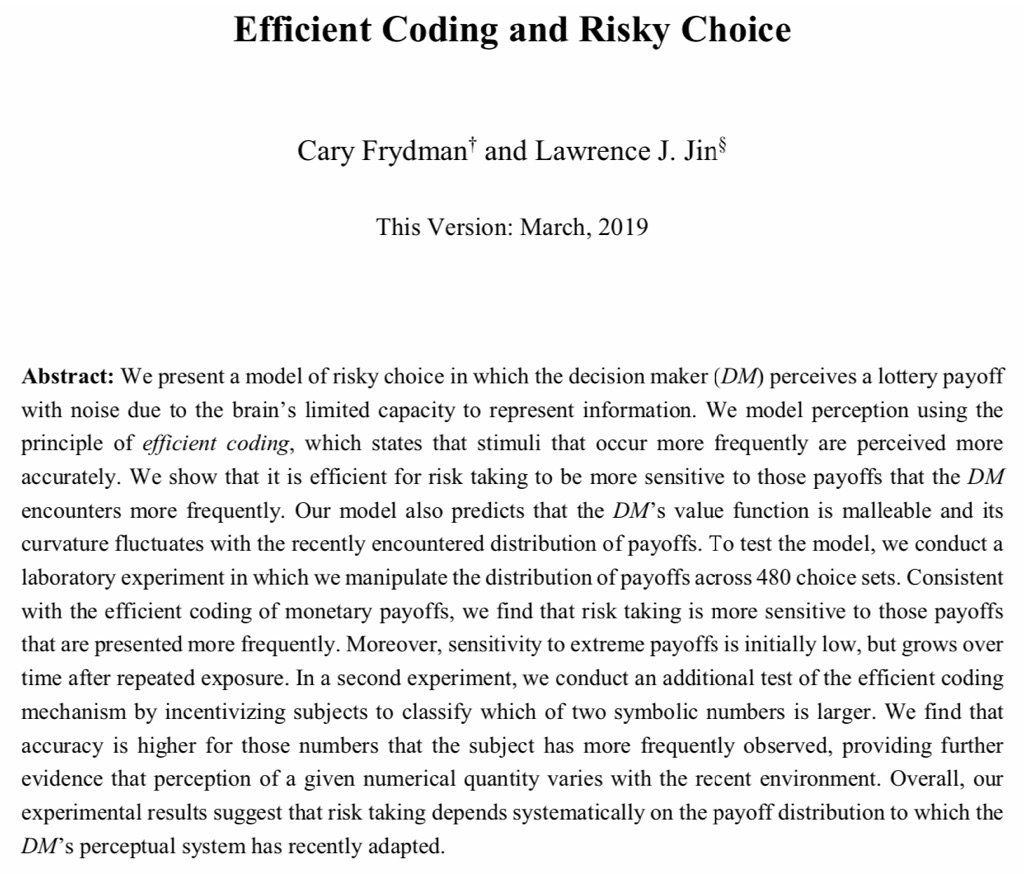

☕️, then PAPER 3: “Efficient Coding and Risky Choice” by Lawrence Jin (@Caltech) with @caryfrydman. Biological constraints on accurately assessing probabilities/payoffs. Model and experiment to understand better how these work! #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 5 Favorites

Mood 0

-

Efficient Coding Hypothesis: brain allocates more resources to stimuli expected to occur more frequently. Model assessed in lab experiment choosing risky lotteries vs safe options. Can generate countercyclical risk aversion. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 6 Favorites

Mood -3 🙁

♻️ 4 Retweets

❤️ 6 Favorites

Mood -3 🙁

-

Intuition per Shimon Kogan discussion: Suppose I have 5 sensors; in low-vol environment I'd put them "close together," in high-vol I'd spread them out more. Can think as helping found - Role of frames in decision making - [In]stability of choice under uncertainty #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +2 🙂

-

Paper focused on comparative statics (i.e., tests of the model), but Kogan sees ability to use the experimental data to estimate model’s structural parameters! (And also suggests some complementary experimental designs.) [See you after lunch] #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +4 🙂

-

Cool decision by our @UKGattonCollege hosts to diverge from standard practice of bringing in a senior prof to give a keynote. Really excited to instead learn from @steve_kempton about the investment properties of thoroughbreds 🐎📈 kemptonbloodstock.com/ #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 6 Favorites

Mood +4 🙂

-

80% of thoroughbred breeding now for commercial market. Gross receipts $377m at Keeneland auction this year with 27 horses selling for >$1m. (Open outcry with reserve prices.) Very different cash flow patterns and risks for males vs female horses. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -6 🙁

-

Auction design: Best horses sold first. (“Every day of the auctions, more private jets leave and more trailers show up.”) Intermediation: Consigner (cf investment bank) takes 5% of sale price—sometimes negotiated. Track takes ~18% of money gambled. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood +2 🙂

-

There are more and more syndicates (pooled investments) with more and more members (4 → 40), but hard to sell tiny stakes in horse partly because lots of payoff is experience of standing in the winners’ circle at the track and can’t do that if you only own 0.01% #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood -1 🙁

-

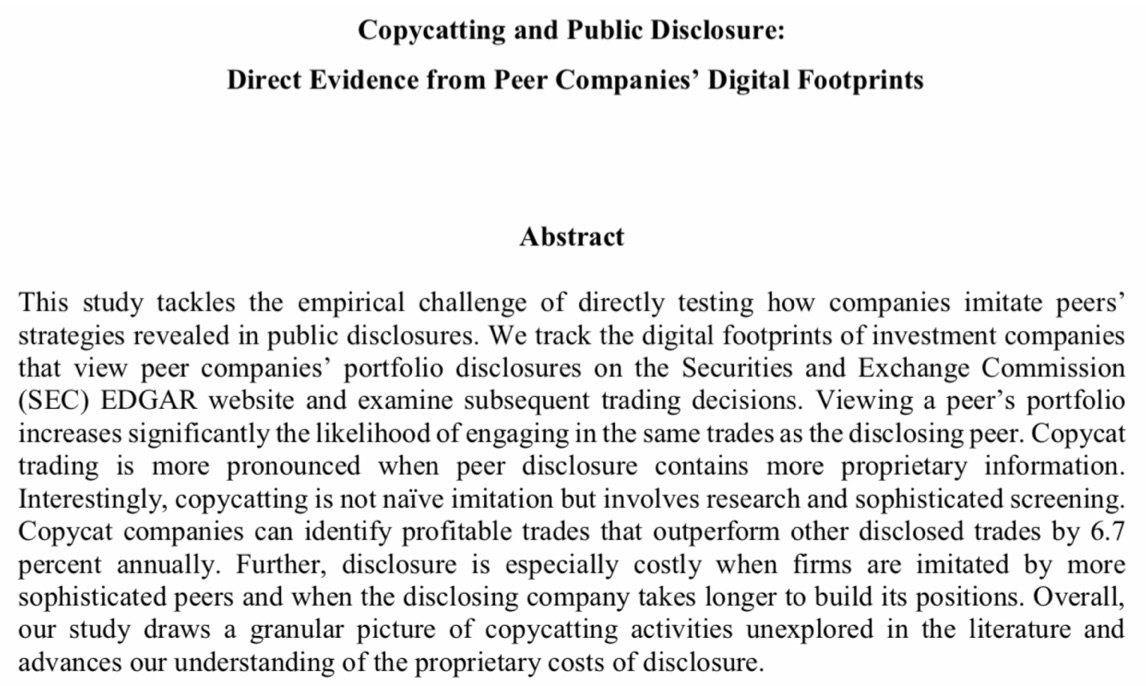

PAPER 4: "Copycatting and Public Disclosure" by Kai Du (Penn State @SmealCollege) with Sean Cao, Baozhong Yang, and Liang Zhang (Georgia State @RobinsonCollege). Asks: Do peers learn from rivals' disclosures, and are copycats naive or sophisticated? #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 2 Favorites

Mood 0

♻️ 5 Retweets

❤️ 2 Favorites

Mood 0

-

Uses IP addresses from EDGAR log files to understand when investment companies view peer firms' portfolio disclosures. Looks like there's copycat trading, which outperforms (!): "sophisticated" humans find the good trades and copy those. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +7 🙂

-

Discussion by (my @WPCareySchool colleague) George Aragon: Some managers complain about having to disclose holdings on 13Fs, and explicit “clone” products like $ALFA exist! (@arpitrage and I have corresponded about this before) @lukestein/1108403587690840064 #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 2 Favorites

Mood 0

-

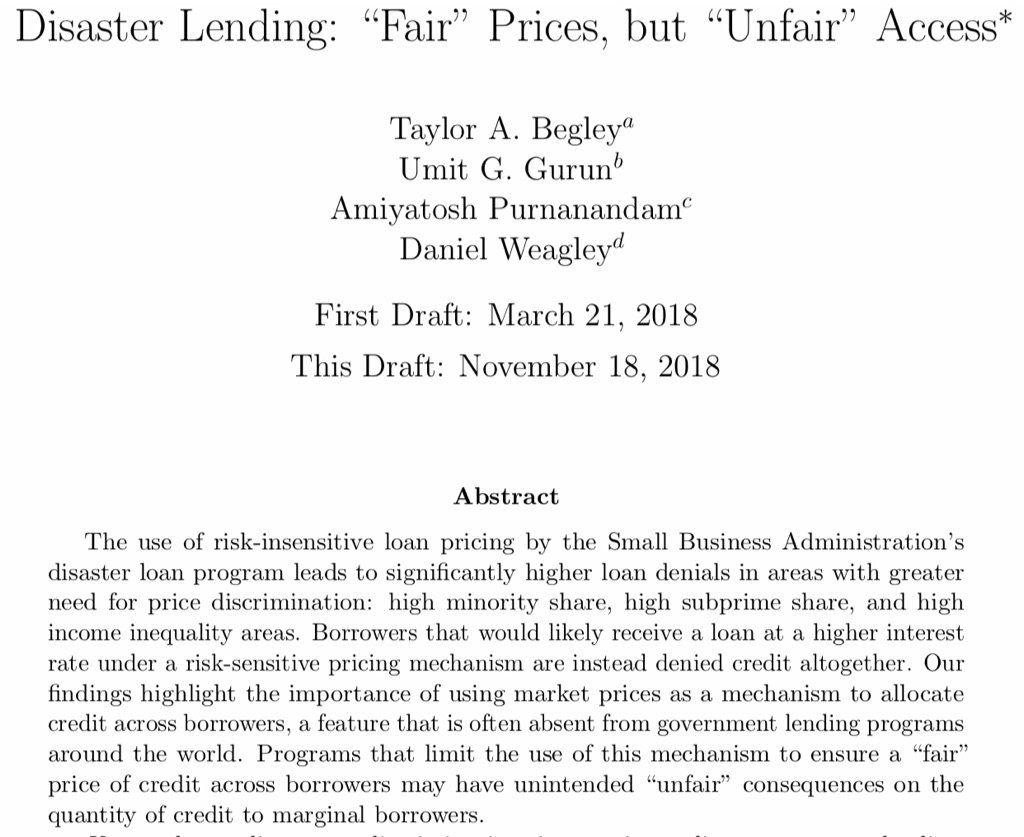

PAPER 5: “Disaster Lending: ‘Fair’ Prices, but ‘Unfair’ Access” by Kentuckian Taylor Begley (@WUSTLbusiness) with @umitgurun, @amiyatosh, and Daniel Weagley (@georgiatechbsch). Asks how removing price discrim affects credit supply (using govt disaster loans) #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 6 Favorites

Mood -2 🙁

♻️ 5 Retweets

❤️ 6 Favorites

Mood -2 🙁

-

.@SBAgov offers subsidized loans to individuals (?!) and business for "rebuilding of non-farm, private sector disaster losses" at the same price (within loan type) for all approved borrowers. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -3 🙁

-

Paper analyzes FOIAed data on ~1.5m loan apps 1991-2015 Find: Fixed-price SBA loans particularly likely to be denied in locations with high minority share, subprime share, or income inequality. But ex post defaults give NO evidence for taste-based discrimination. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood -1 🙁

-

Fixed-prices with screening mean programs may fail precisely the populations programs are designed to serve. Or, as .@startupecon's discussion absolutely nails it with this pithy framing: “Price discrimination without prices leads to discrimination” #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -2 🙁

-

𝔼V < 0 #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 7 Favorites

Mood 0

♻️ 4 Retweets

❤️ 7 Favorites

Mood 0

-

And we're back! PAPER 6: "Unemployment Insurance as a Subsidy to Risky Firms" by @JanisSkrastins with Dimas Fazio (@LBS PhD student), David Schoenherr, and Bernardus van Doornik. Asks: What is the incidence of UI and what are its corporate finance effects? #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 2 Favorites

Mood -4 🙁

-

UI reform in Brazil tightened eligibility requirements for 1st and 2nd time filers but not ≥3rd. Labor supply↓ (known) with stronger effects for riskier firms (contribution). Affects -Employment -Wages -Value particularly of risky firms. Also, entrepreneurship! #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 2 Favorites

Mood 0

-

Very cool: Not just considering heterogeneous effects across risk; using shocks to firm risk from natural disasters propagating through production network. Important (as discussion by Elena Simintzi @kenanflagler notes) because UI can affect risk-taking. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood -4 🙁

-

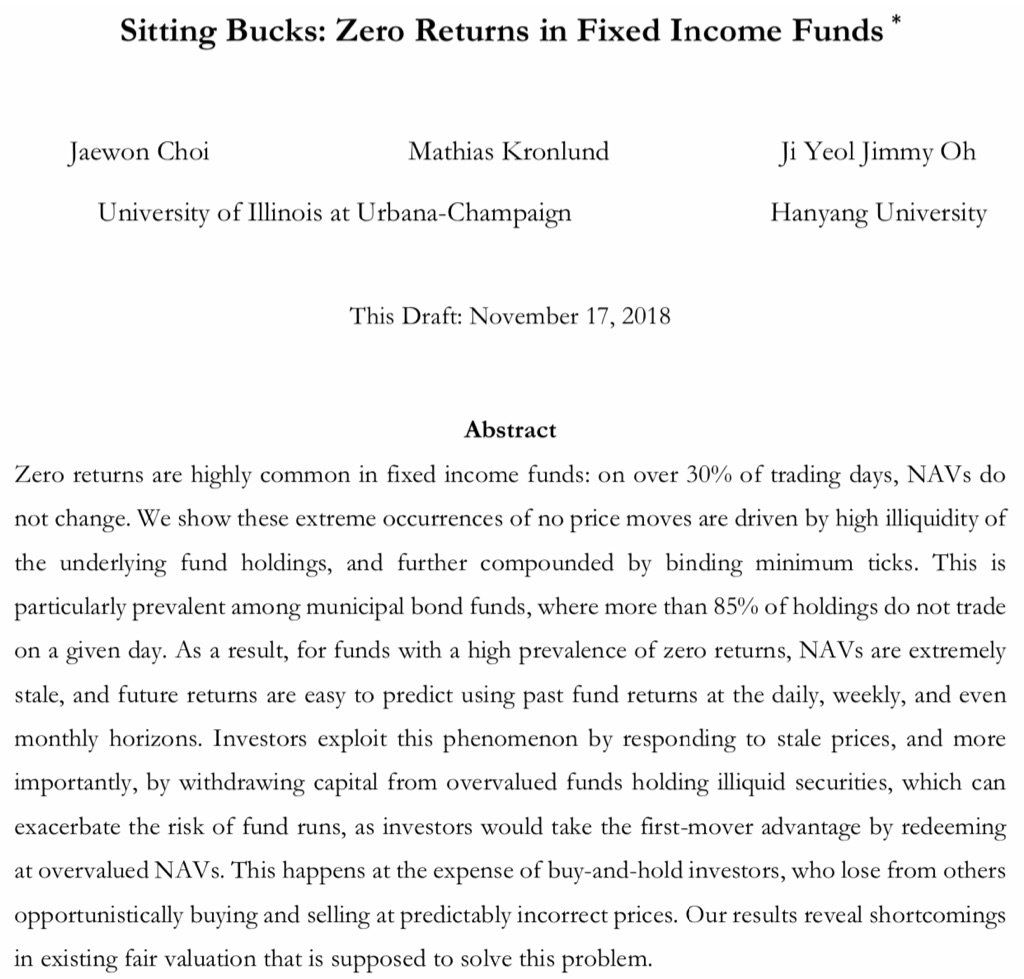

PAPER 7: "Sitting Bucks: Zero Returns in Fixed Income Funds" by Jaewon Choi (@giesbusiness) with Mathias Kronlund and Jimmy Oh (@i_hanyang). Some bonds don't trade for weeks, but mutual funds still have to provide liquidity. Wind up with lots of 0% returns. #KentuckyFin2019Permalink On twitter.com

♻️ 5 Retweets

❤️ 1 Favorite

Mood 0

♻️ 5 Retweets

❤️ 1 Favorite

Mood 0

-

Should use consistent method for "fair value,” but incentives for return smoothing; wind up with "stale" prices. Paper looks at number of zero return days (ZRD) as measure of price staleness (basically <10bps since NAVs center around $10 and tick size one cent). #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +2 🙂

-

Matt Spiegel (@YaleSOM) discussion roughly ranks bond liquidity ("from bad to awful") - Treasury on the run (i.e., newly issued) - Treasury off the run - Investment-grade corporate - NonIG corporate - Distressed - Municipal How do you quote prices? #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -8 🙁

♻️ 4 Retweets

❤️ 1 Favorite

Mood -8 🙁

-

Quotating NAVs using stale bond prices can make a bad problem even worse. [Sidebar: More conference discussions should feature EPIC FAIL Youtube videos. 👏👏👏, Matt] youtube.com/watch?v=KhOCXsOXzIk #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -10 🙁

-

ZRD driven by illiquidity of underlying holdings + minimum tick size Evidence consistent with investors exploiting stale pricing (flow-underpricing sensitivity higher for high-ZRD funds); loads can mitigate this somewhat Increased risk of fund runs #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -3 🙁

-

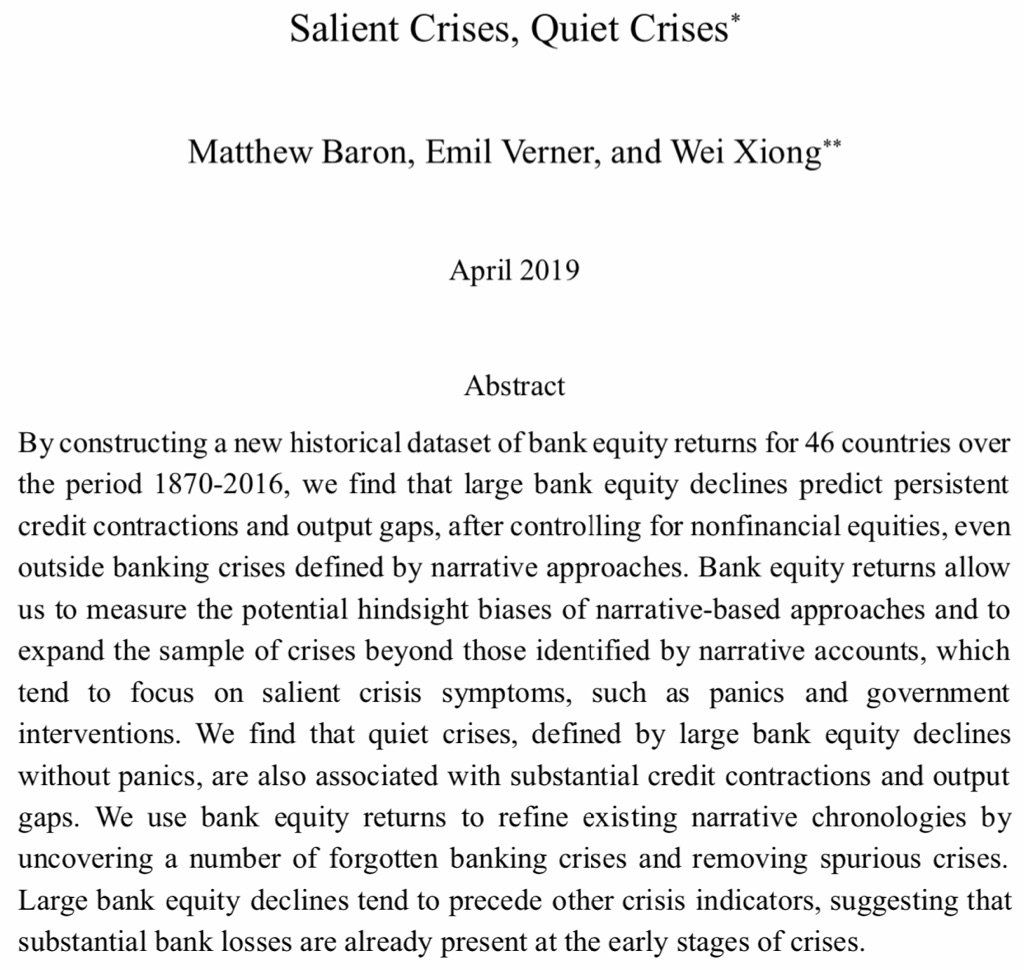

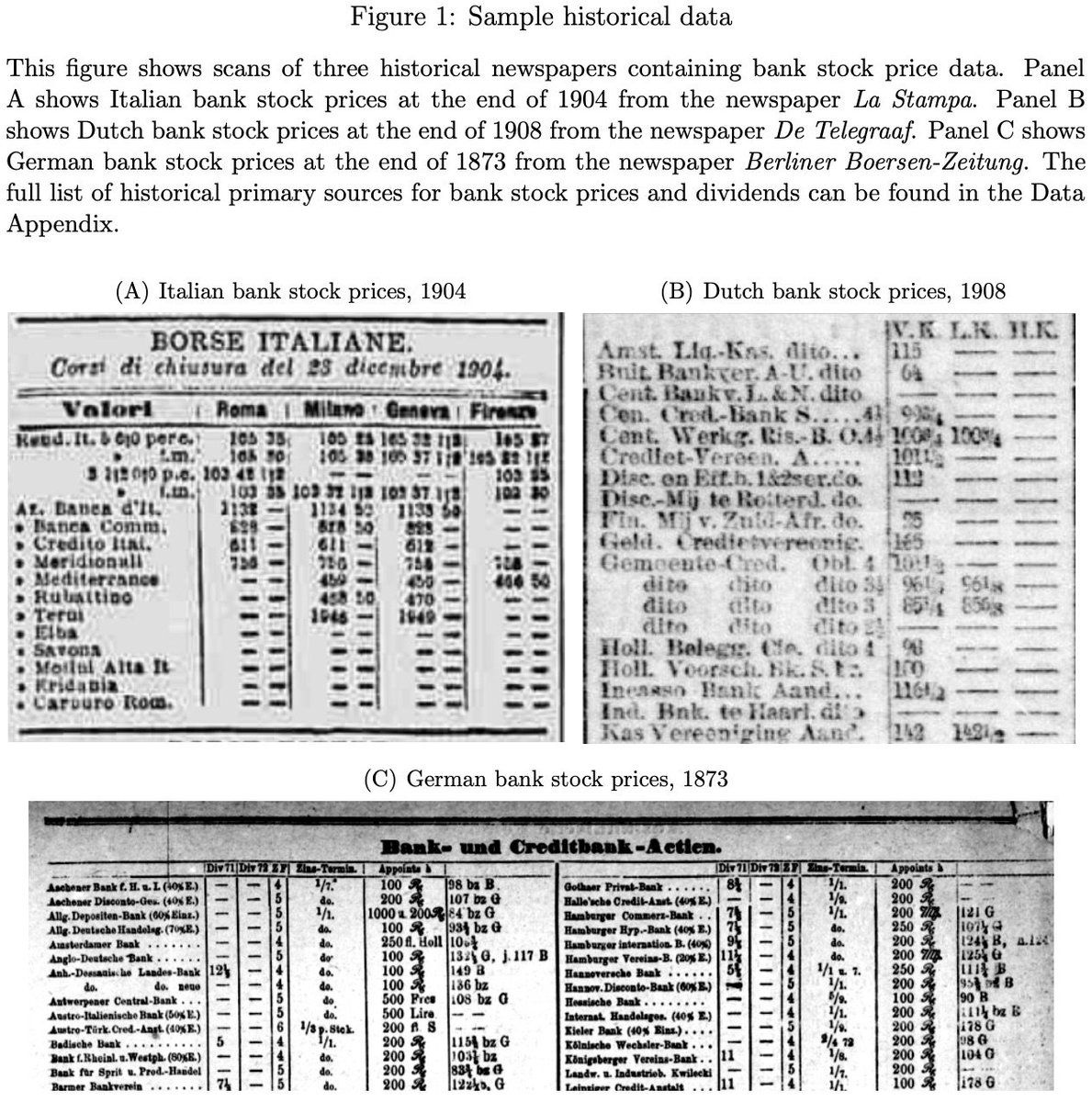

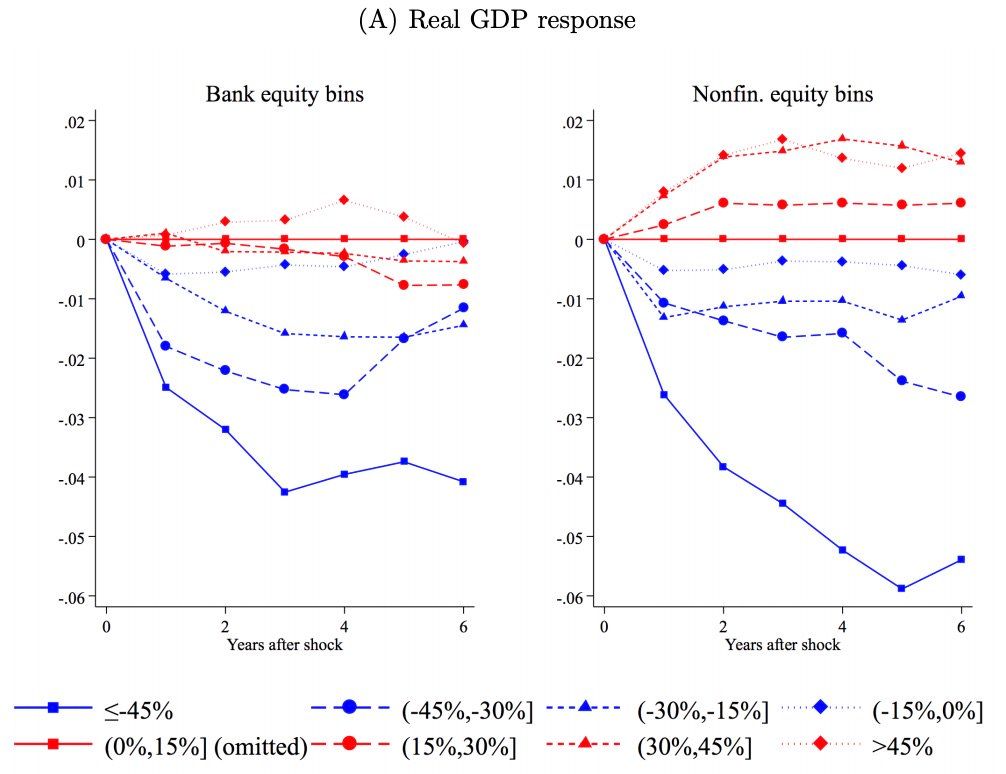

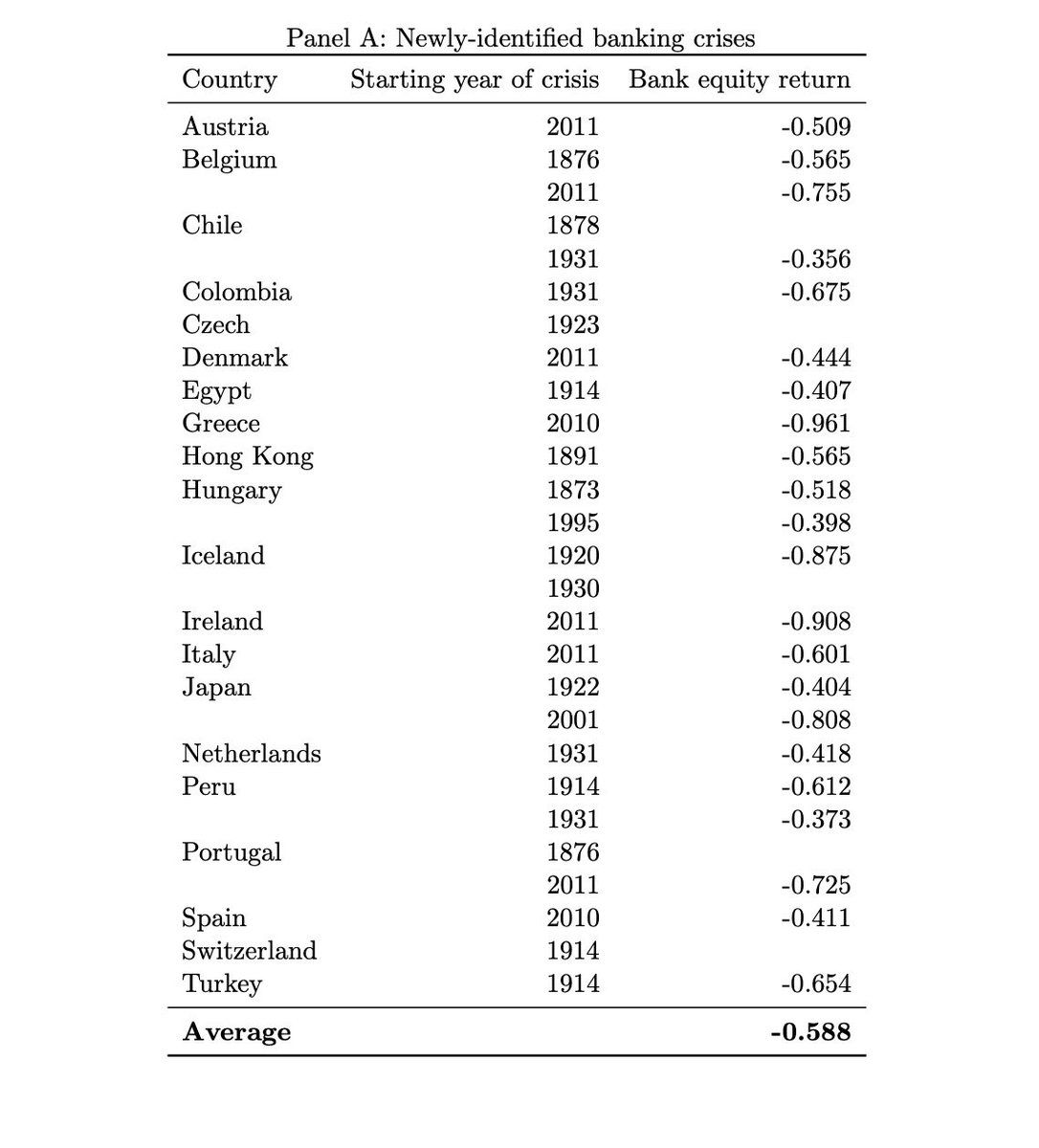

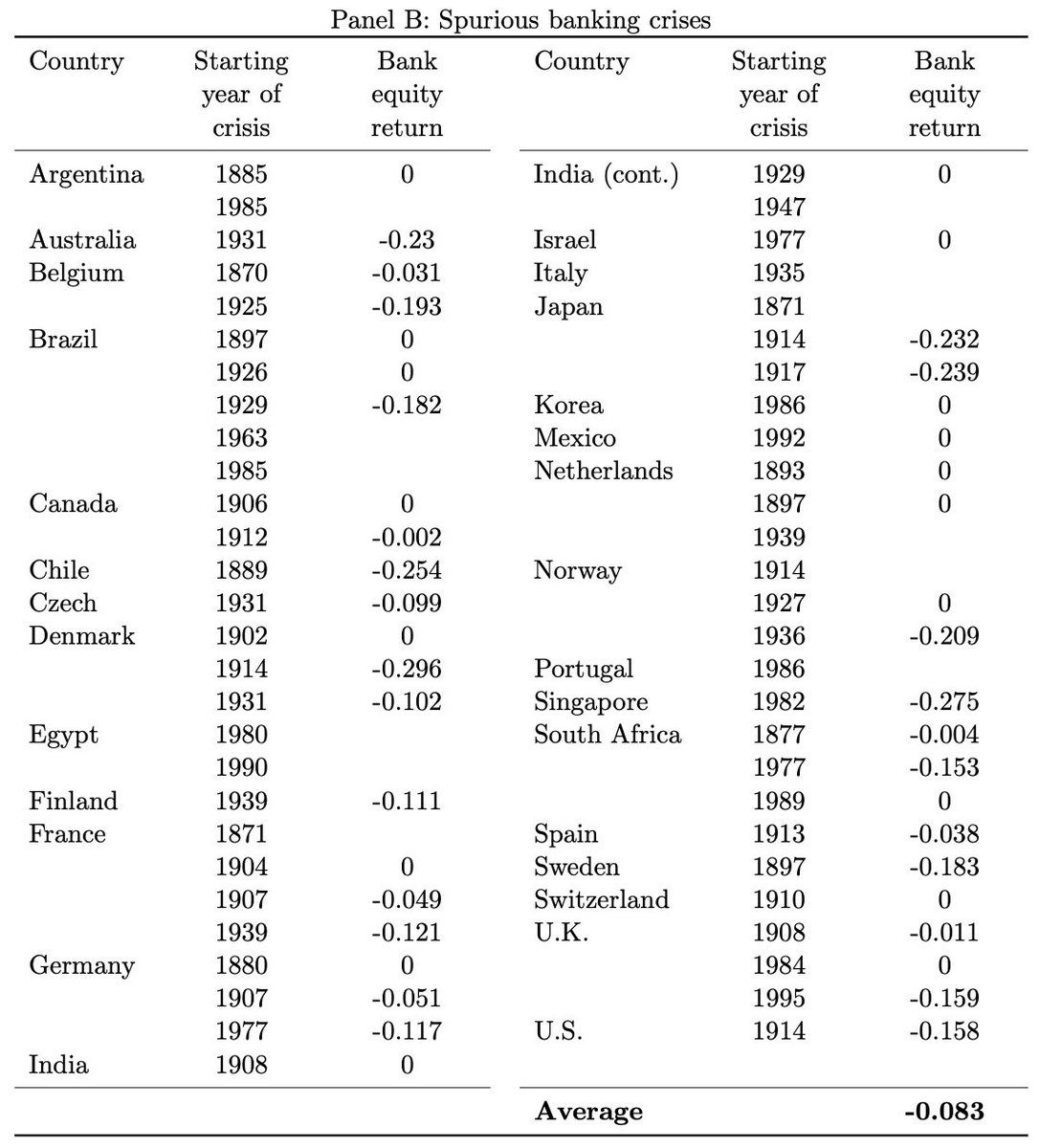

PAPER 8: "Salient Crises, Quiet Crises" by Matthew Baron (@CornellMBA) with @EmilVerner and Wei Xiong [131pp pdf; use wifi] Uses large bank equity declines to identify crises in 46 countries 1870-2016 - Prospective not retrospective - Objective - Quantitative #KentuckyFin2019Permalink On twitter.com

♻️ 9 Retweets

❤️ 11 Favorites

Mood +1 🙂

♻️ 9 Retweets

❤️ 11 Favorites

Mood +1 🙂

-

Very cool new data on bank stock (and non-financial equity) returns. Nonlinear time-series correlations with GDP growth and other outcomes. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 5 Favorites

Mood +3 🙂

♻️ 4 Retweets

❤️ 5 Favorites

Mood +3 🙂

-

Generates a new list of banking crises, and compares with existing “narrative-based” approaches. Bank equity declines precede nonfinancial equity declines and large credit spread increases later, but in older crises, more nonfinancial declines came first. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 2 Favorites

Mood 0

♻️ 4 Retweets

❤️ 2 Favorites

Mood 0

-

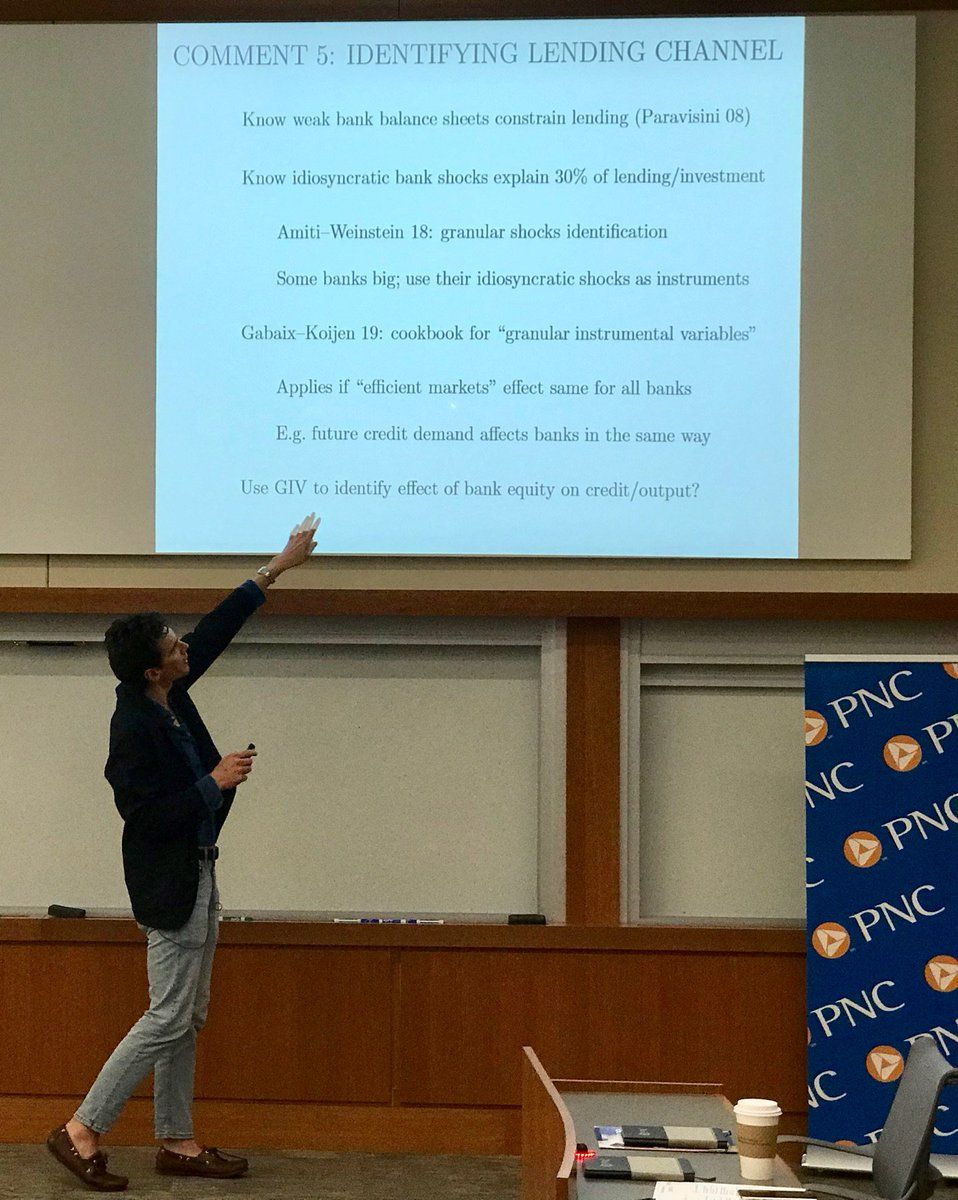

Always love Jason Donaldson’s discussions @WUSTLbusiness; today no exception. Uses Holmström and Tirole 97 jstor.org/stable/2951252 to show why main empirical results aligned with theory, BUT raises questions about efficient markets and identifying channels. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

Mood +2 🙂

♻️ 4 Retweets

Mood +2 🙂

-

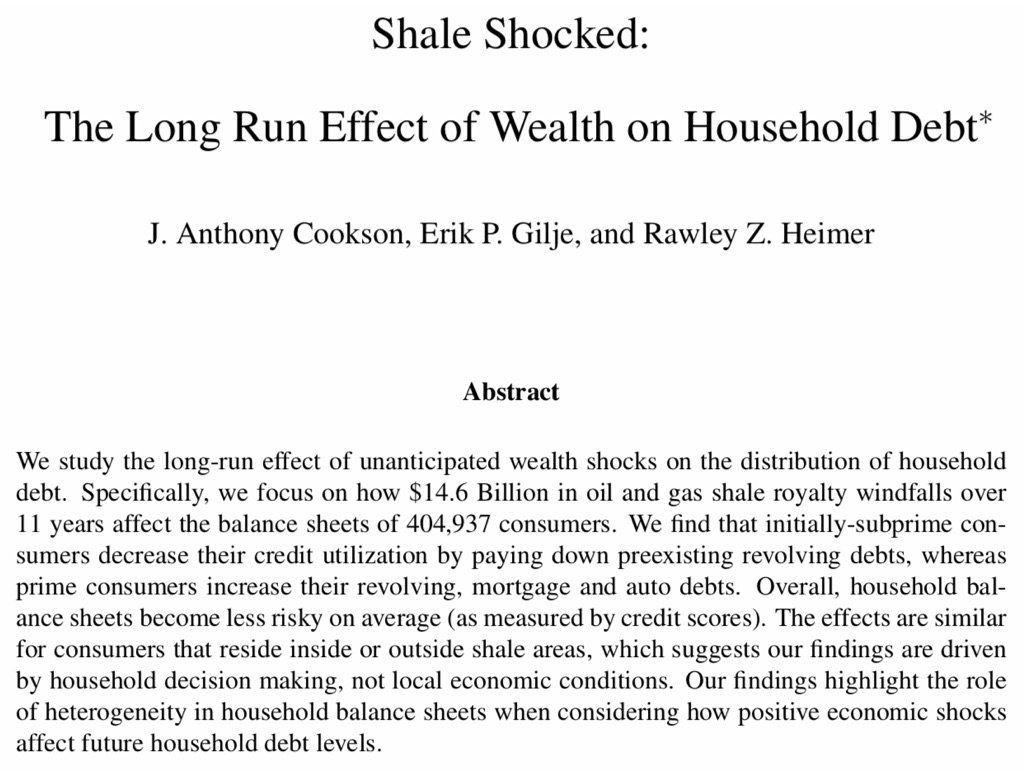

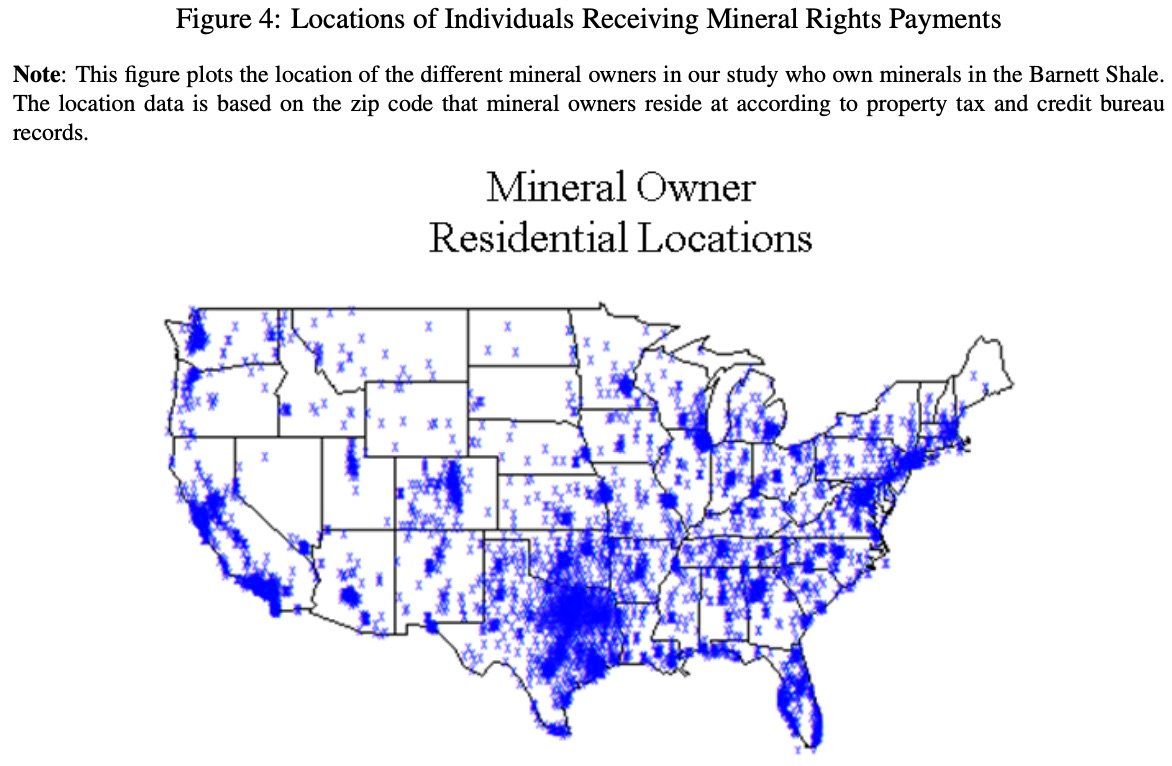

PAPER 9: “Shale Shocked: The Long Run Effect of Wealth on Household Debt” by Rawley Heimer @BCCarrollSchool with Cookson @leedsbiz and Gilje @Wharton. How does wealth affect debt? Experian credit profiles matched to 400k HH receiving $15B in oil/gas royalties. #KentuckyFin2019Permalink On twitter.com

♻️ 8 Retweets

❤️ 3 Favorites

Mood +2 🙂

♻️ 8 Retweets

❤️ 3 Favorites

Mood +2 🙂

-

Royalty rights dispersed and shale fracking took industry by surprise. DiD effects of wealth shock vary with credit score - Subprime: ↓ revolving and mortgage balances - Prime: ↑ revolving, auto, and mortgage balances Effects level off at ~$50K wealth shock #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +2 🙂

♻️ 4 Retweets

❤️ 1 Favorite

Mood +2 🙂

-

PAPER 10: My presentation (can’t tweet): “Financial Inclusion, Human Capital, and Wealth Accumulation: Evidence from the Freedman’s Savings Bank” (with Constantine Yannelis). ssrn.com/abstract=3302996 Excited for discussion from Jordan Nickerson @BCCarrollSchool #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 5 Favorites

Mood +7 🙂

♻️ 4 Retweets

❤️ 5 Favorites

Mood +7 🙂

-

Home stretch; PAPER 11: “Leverage Risk and Investment: The Case of Gold Clauses in the 1930s” by Mete Kılıç @USC with Joao Gomes @Wharton and Sebastien Plante @WSBresearch Considers a channel for gold standard→corporate investment during Great Depresn recovery #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 2 Favorites

Mood +5 🙂

♻️ 4 Retweets

❤️ 2 Favorites

Mood +5 🙂

-

Looked like FDR might devalue dollar by raising gold prices, but many bonds (≈2x️ GDP) had “gold clauses” denominating payment in gold! Gold clauses abrogated in 1933, upheld by Supreme Court 5-4 in 1935. #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood +12 🙂

-

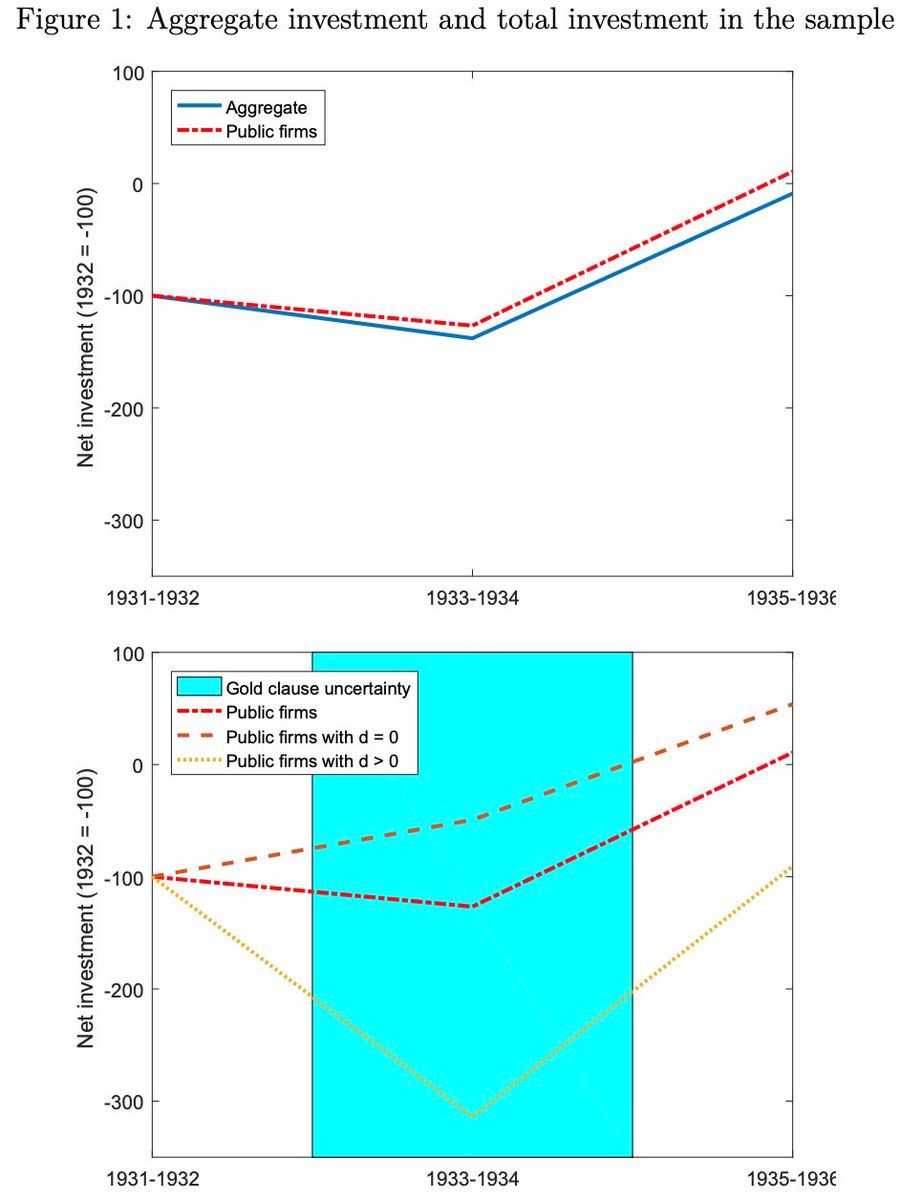

Estimates diff-in-diff of firms w/wo gold clause bonds using new data on firms' bond terms 1931-36. 5% lower investment for affected firms with expected later reversal Implications for interplay between exchange rate uncertainty, nominal debt, and deflation risk #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -3 🙁

♻️ 4 Retweets

❤️ 1 Favorite

Mood -3 🙁

-

Discussion by Sudheer Chava @georgiatechbsch asks about tests that can help separate channels: (1) Credit supply, (2) leverage risk/debt overhang (3) fundamental uncertainty. Some channels have more contemporary relevance. #KentuckyFin2019On twitter.com

♻️ 4 Retweets

❤️ 1 Favorite

Mood -2 🙁

-

And… that’s a wrap. Another awesome conference in the books. Sadly, my flight home meant missing the optional post-conference bourbon tasting [photo credit: Kristine Hankins] so had to do my own at the airport. Thanks so much to our @UKGattonCollege hosts! #KentuckyFin2019Permalink On twitter.com

♻️ 4 Retweets

❤️ 9 Favorites

Mood +2 🙂

♻️ 4 Retweets

❤️ 9 Favorites

Mood +2 🙂